The process of input and output that follows the processing of the data is referred to as the IPO cycle, as implied by the title. First, the input is given for the output, and then the input needs to be processed to get the results you want. By issuing shares to the general public, businesses can use an Initial public offering (IPO) to raise equity capital. Or, existing shareholders can trade their stock to the public without acquiring additional capital.

A company is considered private prior to an IPO. Since it was a private company before it went public, it has grown with a small number of shareholders, including professional investors like venture capitalists and angel investors as well as the founders’ family and friends.

During an initial public offering (IPO), the company’s shares are valued through underwriting due diligence. Private shareholder shares are valued at the price of public trading when a company is listed on the stock exchange, converting previously held private shares to public ownership. Private and public share conversion provisions may also be included in share underwriting.

Going public can be a daunting, time-consuming, and difficult process for businesses to manage on their own. In order to comply with the requirements of the Securities and Exchange Commission (SEC), which is the body that oversees public companies, a private company that plans to go public with an initial public offering (IPO) should not only prepare for an increase in public scrutiny but also submit a large number of financial and legal documents.

This is why a private company that wants to go public hires an underwriter, usually an investment bank, to advise on the IPO and help figure out how much to charge for its offering. By arranging meetings with potential investors and preparing important documents for investors, underwriters help management prepare for an IPO. Roadshows are the names given to these gatherings.

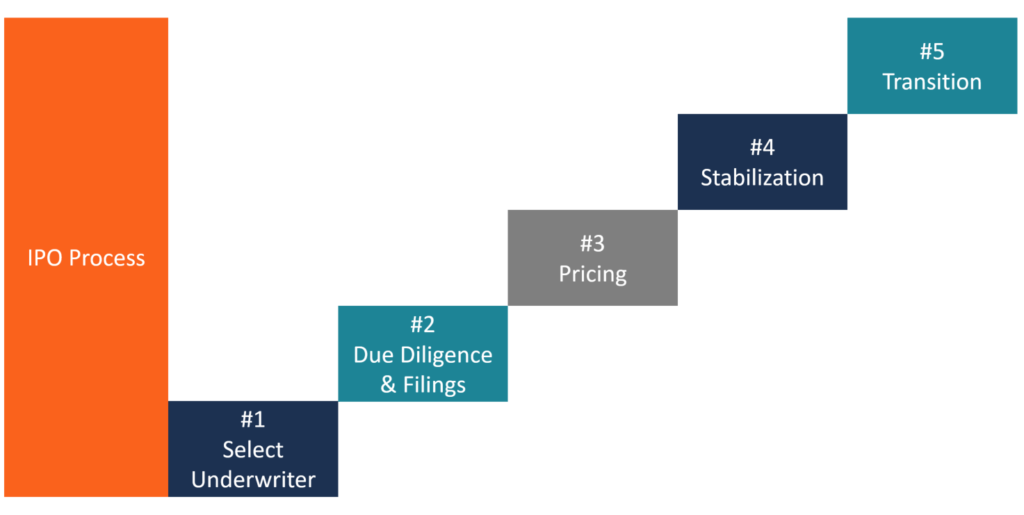

The company will enlist the assistance of financial professionals, such as investment banks, in order to initiate the initial public offering process. The company is reassured by the underwriters, who also act as a link between the investors and the company.

Along with the draft prospectus, which is also referred to as the Red Herring Prospectus (RHP), this IPO step requires the preparation of a registration statement. The Companies Act mandates that RHP be submitted. This document contains all of the SEBI and Companies Act disclosures that must be made.

After that, the company’s disclosure of facts is checked by SEBI, the market regulator. The company can announce a date for its initial public offering (IPO) if the application is accepted.

Roadshows are used by the company to try to get attention in the market before an IPO goes public. The company’s executives and employees will promote the upcoming IPO across the country for two weeks. Basically, this is a marketing and advertising strategy to get investors’ attention. Diverse individuals, such as fund managers and business analysts, are informed about the company’s most significant features. Questions-and-answer sessions, multimedia presentations, group meetings, online virtual roadshows, and other user-friendly methods are utilized by the executives.

The fact that the company is able to obtain investments from the general public in order to fund capital is one of the main advantages. This facilitates acquisition transactions (share exchanges) and enhances the company’s exposure, popularity, and public image, which may increase the company’s sales and profits.

A business may be able to obtain better terms for credit borrowing than a private company due to the increased transparency provided by the requirement for quarterly reporting.

When they go public, there are a number of drawbacks, and they may choose different tactics. The main drawbacks are the high cost of an initial public offering (IPO) and the ongoing costs of running a public company, which are typically unrelated to other business-related costs.

Management may be evaluated and compensated based on stock performance rather than actual financial performance because the price of shares may be distracting. Financial, accounting, tax, and other information about the company must also be made available by the business. The company may be required to disclose business secrets and strategies that may assist competitors in these disclosures.